Nothing is more fun than tribalism. Watching a sports match is one thing, yelling abuse at those who happen to support the other team for no other reason adds that extra little sizzle to the experience that really keeps us coming back. The human mind – forged in the nasty, brutish and short lives of antiquity, has a slot designed for loving those who share our practices and values – and hating those who don’t – regardless of whether there’s any merit or reason to that. And that, my friends, is the pinch of salt that you’ll have to take when you hear me say this: We in the rates market know what those equity monkeys can’t know – and don’t know – that this economic cycle is almost done, and the great asset valuation bear market is about to draw down on us with a vengeance.

A bit of background for those of you who need a grounding in the different tribes here, let me lay out the two stalls. In the rates market, we try and figure out the fair valuation of a $ tomorrow vs a $ today. How and why those $ end up in different folks pockets is not something that interest us. We trade promises to pay later, made by governments or companies, or aggregated promises of individuals – but at the end of the day our intellectual muscle is spent figuring out the fair value of those promises. If the US government promises you a $ in 10y time, what’s that worth today? The zero coupon 10y yield is, according to ijamlon 1.789% – so about 84 cents. 5 years ago in 2011, the 10y rate was closer to 3.75%, so a dollar from the US government was worth 69 cts upfront. What changed? Did the US government get more creditworthy? Given they own the printing press that seems implausible. Did we all start saving more?

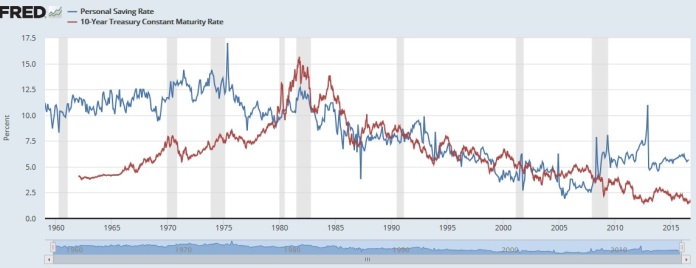

Eyeballing that chart, no, in 1011 the savings rate was about 5% and it’s about 5% now – yet we value $ in 10y time 20% more than we did back then. So what gives? That’s what I spend my professional life worrying about.

What Equity market professionals worry about is quite different. Rather than the price of a $ now vs that in 10y time, they worry about trying to buy up quasi ownership rights of what they believe are the good bits of the real economy. When you buy equities, you’re paying for the income stream that some particular arrangement of labour and capital – embodied in a company is going to provide you down the line. Equity guys are all about the process of production – trying to anticipate the way the world will change, and trying to keep invested in those companies that will deliver returns. It’s not about when the $ come, because if you invest in the right capital/labour arrangement – you’re not buying cashflows you’re buying the right to participate in the cashflows that result from the success of those arrangements. And you know that in the background, the rates guys are hard at work making sure that whenever those returns are coming, they’re fairly discounted back into today’s money so that you get the benefit in price terms. It’s a very different activity. Equity guys aren’t thinking about when and how they get paid. The market takes care of that. They’re thinking about whether companies are succeeding or failing.

What prompts me to write this is a chart I made last week. I encourage you to go look at it yourselves. Plot the performance of any measure you like of “Growth stocks” (I used an ETF, DM me for the ticker, I don’t have it home) – and charted it as a ratio to the SPX to measure relative performance. I then put the slope of the 2’s10’s curve in $ on the same chart. Let’s back up. What’s a “Growth stock”? Well, basically, it’s a stock where you’re expecting that by investing a lot upfront – the company is going to reap substantial returns in the future. In other words, you’re paying someone to invest money in real assets for you to generate income. Those stocks have outperformed. At the same time, 2’s10’s – the slope between the 10y rate and the 2y rate in the US has crashed out of a range it held for a few years, and sits around 50bp where it was previously moving around between 100-250. What are those two things telling you?

In one sense, it’s the same thing. Both rates people and equity people are “long duration”! The rates people have decided that it’s only 0.4% worse, per year, to lock up your money for 10y rather than 2 – ie they’re happy to get their money later. The equitiy guys are thinking the same! They’re after growth stocks – stocks where the stream of dividends that are ultimately what the investors have to live on are a long way out. But then, in another very important respect, it’s not the same at all. Growth stocks are only going to pay dividends if they are allocating capital well- and therefore future rates of return on capital are high. But the rates market is telling you that in the future, the fair rate of return on capital is going to be low. Historically, a flat yield curve is a good predictor of a recession.

My partisan read of this is that the equity market has been forced, in the absence of any real ability to predict future returns and especially recessions to bid up duration. The difference is, we in the rates market know they’re doing it and I don’t think they do. And the other difference is that their “duration” is “future claims on REAL returns” of companies – whereas our duration is just fixed cashflows. In summary, the rates market is telling them they’re about to fall and fall hard – yet due to myopia, optimism and unfounded bullishness – that very same force is pushing equity valuations to new highs. All of this unwinds in an ugly way.